Top US Stock Results Interpretations

TSMC Results | Challenging Historical Highs, AI Competition's Biggest Gainer?

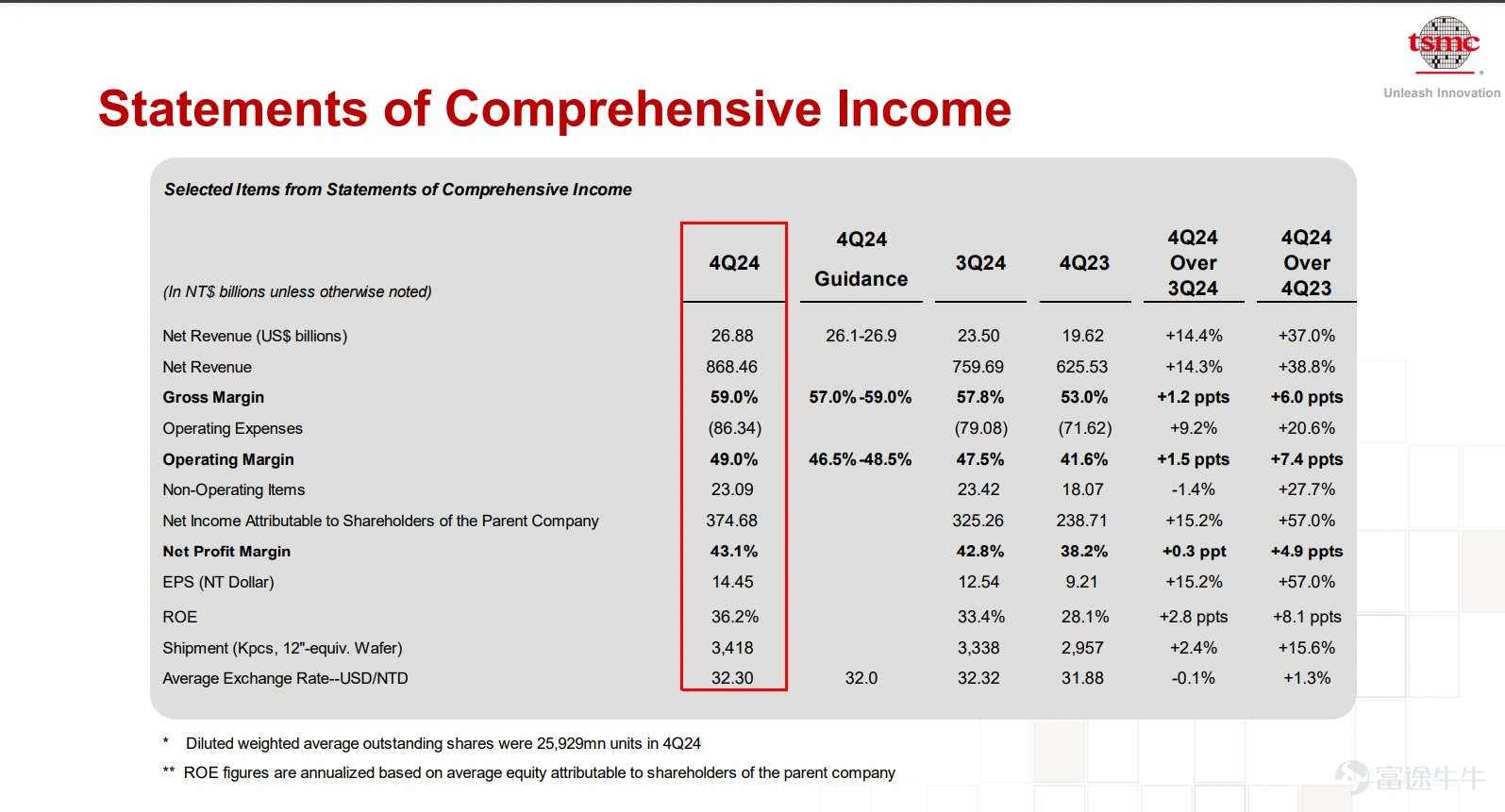

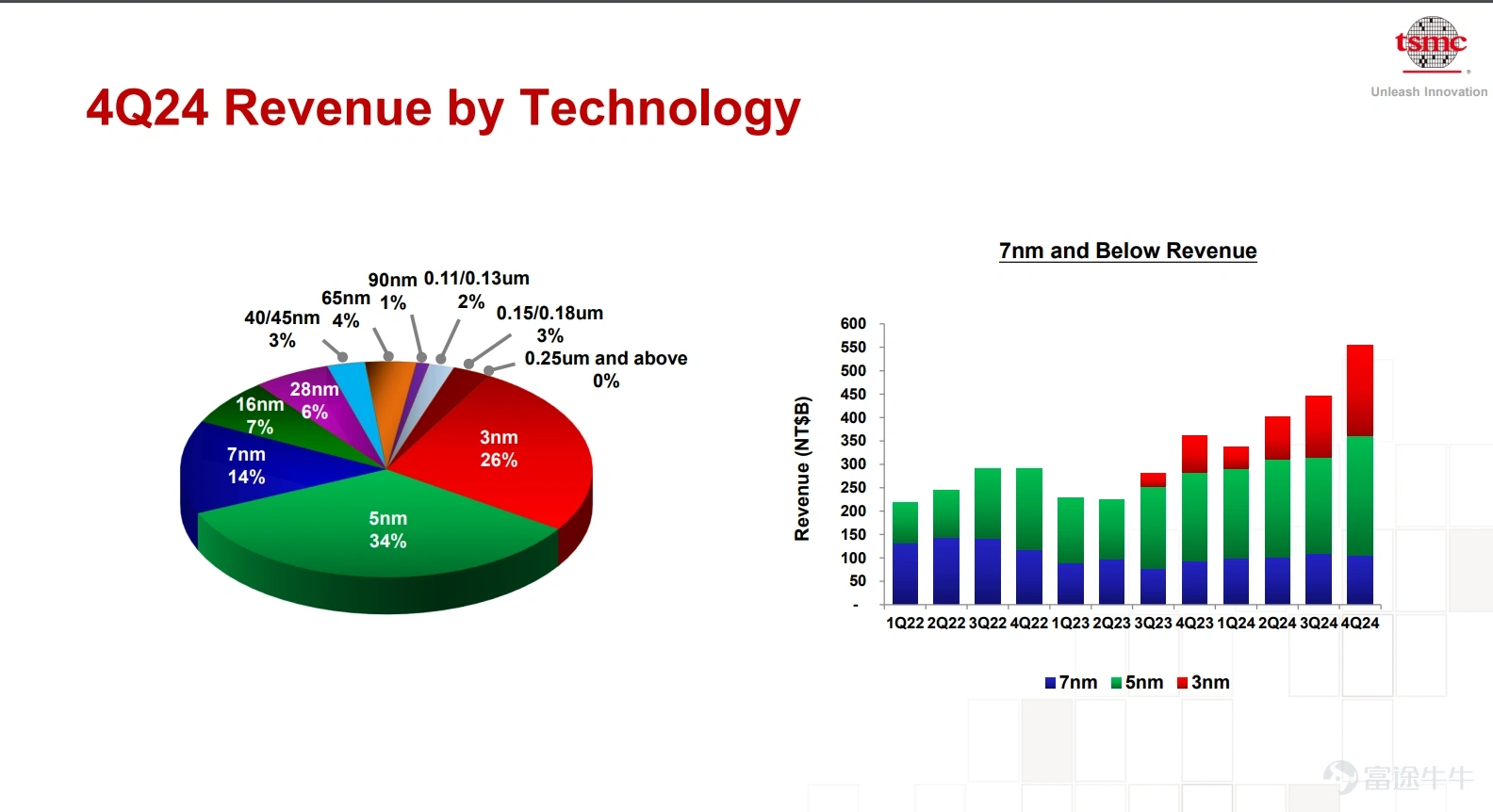

$Taiwan Semiconductor(TSM.US)$ Announcing Q4 results, the company's revenue continued to grow strongly, with Q4 2024 revenue of NT$868.461 billion, up 38.8% year-on-year; net profit of NT$374.68 billion, up 57% year-on-year; and diluted earnings per share of NT$14.45. Benefiting from the demand for computing power for high-end chips in the AI developing market, the company's 3nm shipments increased from 20% to 26% in Q3. This is the main reason that drove the company's gross margin to 59%, the upper end of the gross margin guidance of 57% to 59% for the fourth quarter of 2024. In addition, the company's ability to control costs was strong, and the operating margin increased to 49.0%, which was stronger than the previous quarter's guidance of 46.5% ~ 48.5%. Reflecting on TSMC's strong R&D capabilities, its ability to control costs should not be overlooked.

TSMC Performance Interpretation

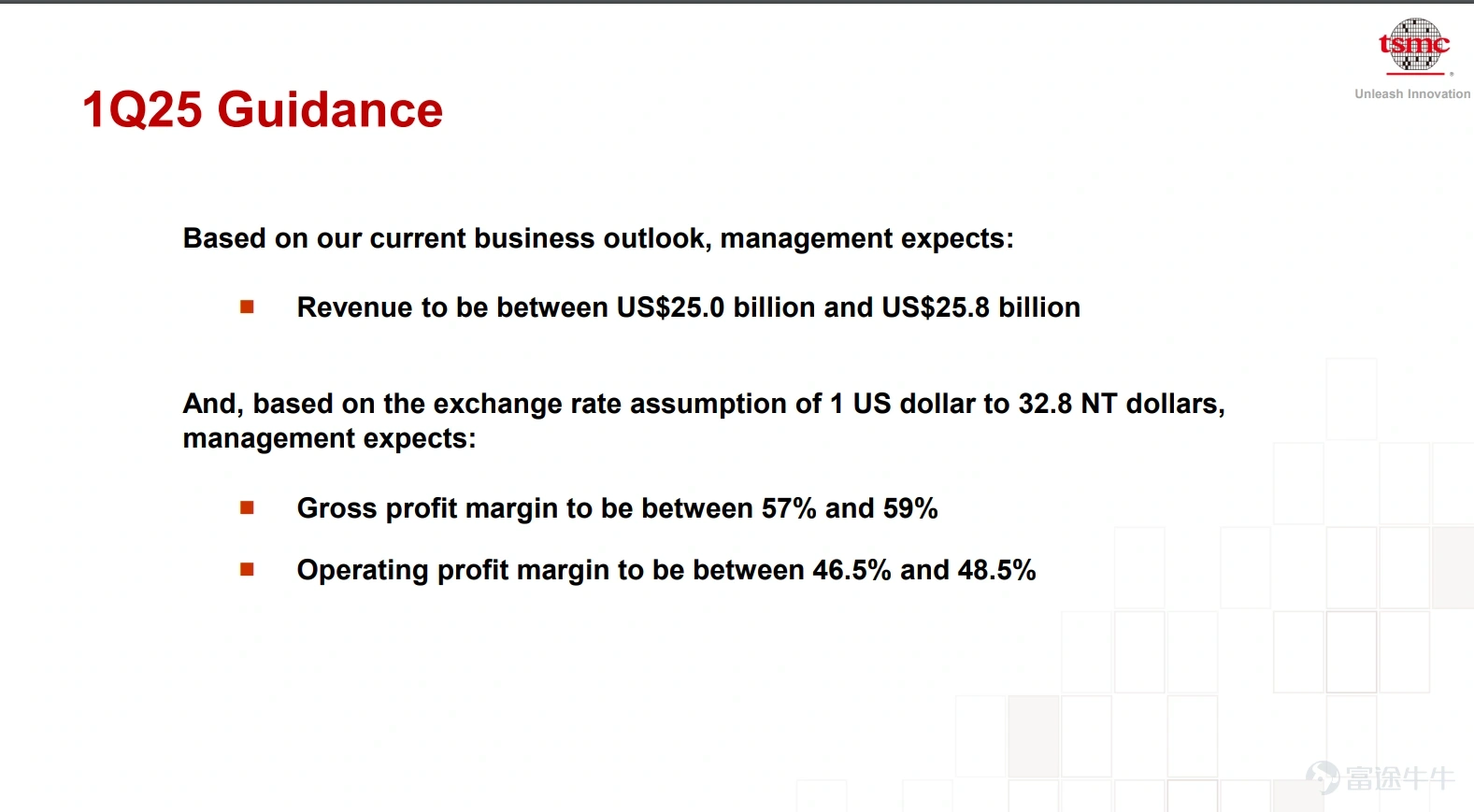

In this year's Q1 (1Q25) guidance, the company expects first quarter sales of $25 billion to $25.8 billion, higher than the market estimate of $24.43 billion. In USD terms, sales will grow by around 25% in 2025. The first quarter gross margin is expected to be 57% to 59%, which is 56.9% higher than the market forecast.

Operating Data

Considering that the market demand for high compute is still very large and there is no threat from competitors for the time being. And supported by AIPC and the new smartphone's AI capabilities, the benefits of momentum demand will be directly reflected in TSMC's performance.

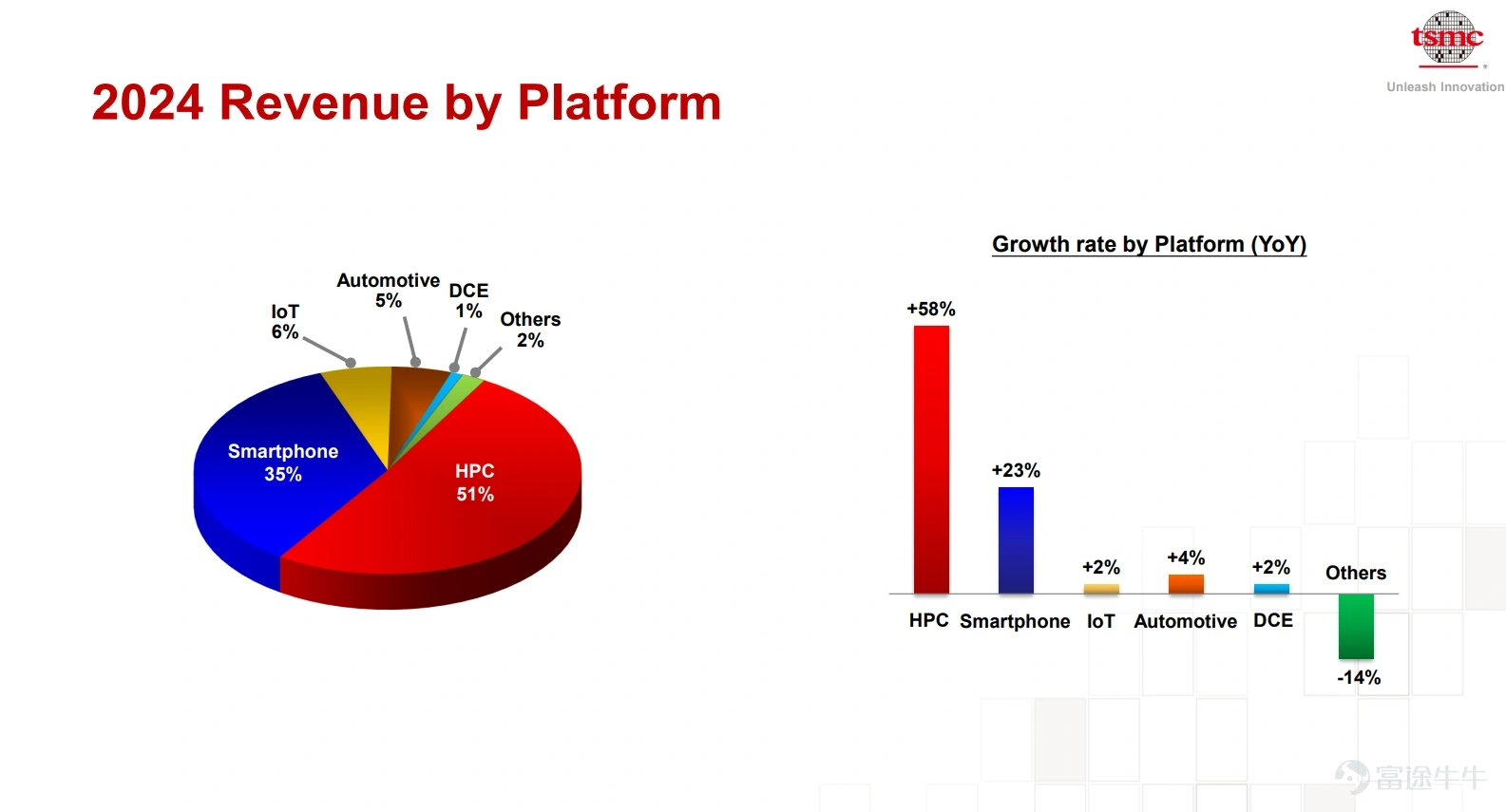

It is clear from TSMC's wafer revenue distribution above that the 3nm share is expanding, which is the main reason for TSMC's continued high gross margin and strong bargaining power.

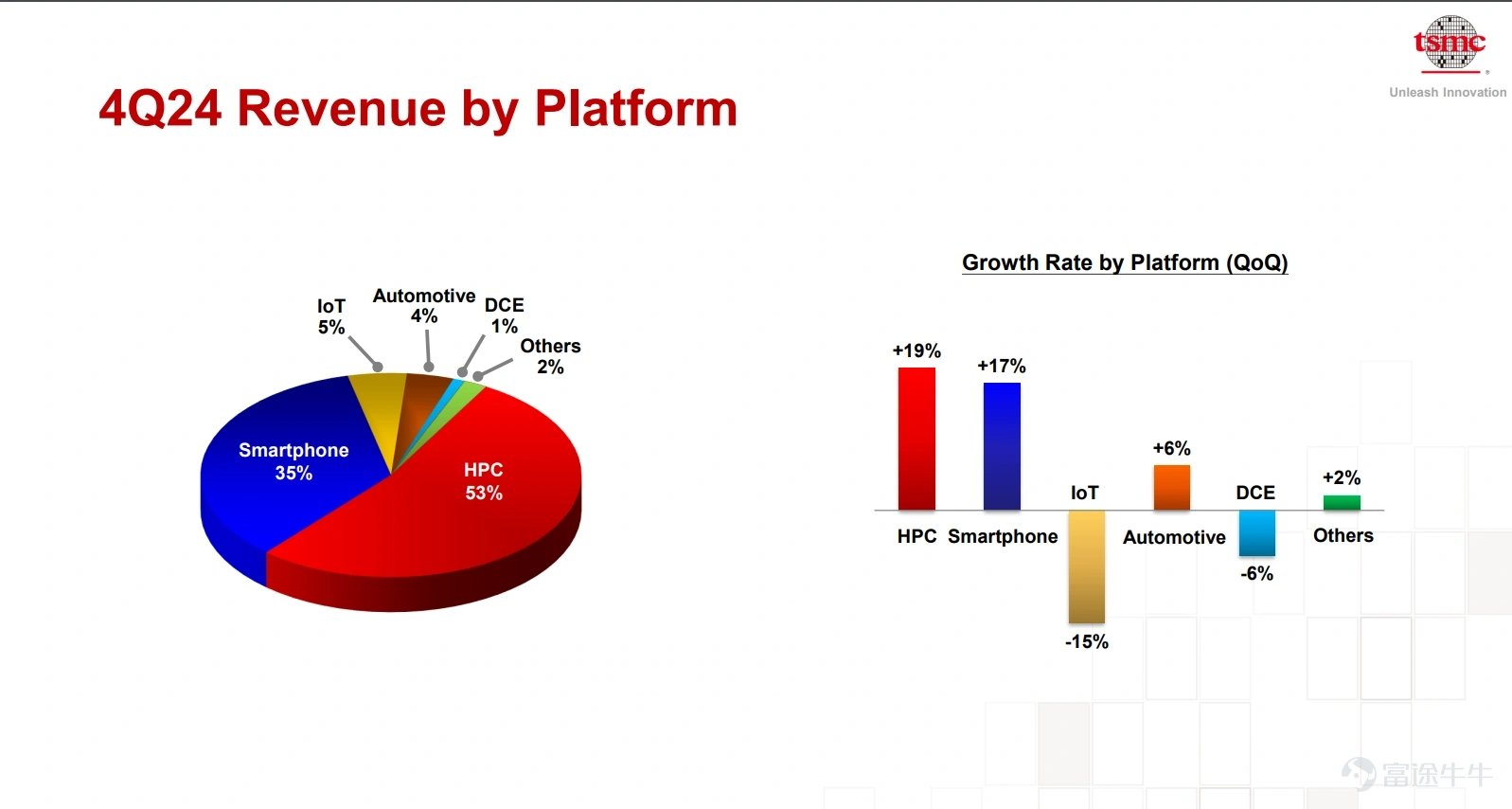

It is also clear from the chart above that high-performance computing (HPC) and smartphones remain the main drivers of growth on a quarterly and year-over-year basis. Given that there will still be many tech giants vying to build or upgrade AI data centers this year, TSMC is one of the biggest beneficiaries of the global AI development competition, there is no question.

Determination of TSMC Stock Price Results

We will use several angles to judge the stock price movement after the results:

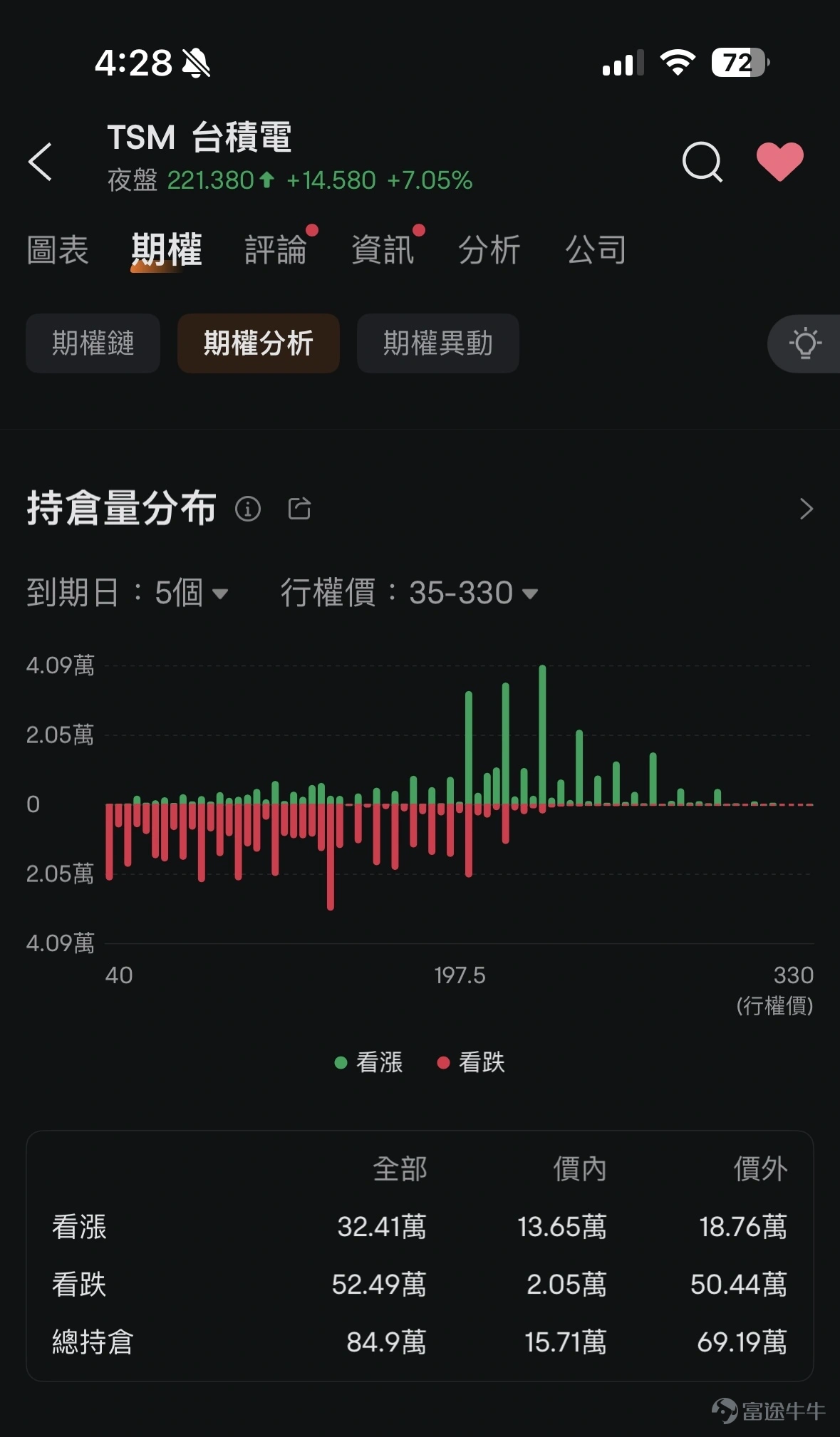

1. Option Distribution

Supported by strong results, the share price is expected to break through the high of $222.2. First, you can take a look at the stock position announcement for the options, and first look at the 5 positions breakdown for the most recent “Expiration Date”:

It can be viewed on Futubull phones, TSM->Options->Options Analysis->Hold Stock Breakdown. The most recent 5 call options were divided between $200, $210 and $220, with $220 being the most heavily traded at around 0.0409 million, which would amount to $0.9 billion at the current price of 100 shares and $220. You don't have to show a lot of clingy air warehouse behavior when you look at the Pythoplane heads. The $220 position will be a valuable reference.

2. Valuation Level

Reference the valuation levels of the past 5 years (the reason for 5 years is that AI is only a technology that has developed in recent years, it becomes too far inaccurate). The company's average market earnings over the past five years are approximately 26.9 times. With earnings per share ADR of $7.04 in 2024 results, the overnight listing price of about $220 at the time of writing is approximately 31.25 times market earnings. This figure is still below the estimate of about 35 times the 5-year average of about one standard deviation above. Given that TSMC's current profit growth space and development story remain very good, the authors consider the current valuation to be reasonable and attractive, even conditional to a level of 1 standard difference of around $246.

If the development of AI accelerates further this year, further straining the overall demand for momentum, the most bullish target price could reach two standard spreads of 42.6x market earnings, or close to $300.

3. TSMC Technology Analysis

The share price has remained on a short-term upward trajectory since December, and the share price has performed better than the US stock market $S&P 500 Index(.SPX.US)$ und $Nasdaq Composite Index(.IXIC.US)$ 。 From the bullish track reference, it can be judged that $200 will be a key support position. The share price hit a high of $222.2 on January 6 this year, closed at $220.1 on the day, and then broke through on January 7. $220 will be a more critical resistance in the short term. If today's results break above this threshold, it will be favorable for the stock price to continue to hit new highs in the aftermarket. This view and options analysis are compatible.

In addition, the technical indicator MACD will form a “double bull” pattern if the position is able to signal a gold cross at a high level, which is a more favorable mid-term bullish signal.

Key Dividing Range (can be a support position or a resistance level): $220

KEY SUPPORT LEVEL: 200 YUAN

KEY RESISTANCE LEVEL: N.A. (BREAKING THE TOP WILL LEAVE NO CRAB SUPPLIES)

TSMC Investment Strategy Recommendations:

All in all, whether the share price can break above $220 in the short term will be a key factor. If a commodity investor is in possession, it is recommended to continue holding under the support of strong fundamentals. If you do not want to buy a commodity, consider a strategy of sell and sell options for the time being, earning the option money and deploying it to avoid the risk of a sharp rise in the stock price. If you're buying a major stock right now, it's best to adopt a mid-line investment mindset, or make a split bet with both hands ready.

Author Information

Chief Analyst of Futu Securities Liang

(Source: Company Reports)

(The author is a licensee of the Securities and Exchange Commission and its affiliates do not have any financial interest in the Proposed Share Issuer)