Top US Stock Results Interpretations

AI Business Has Failed, Continued Bullish After Yakuba Performance?

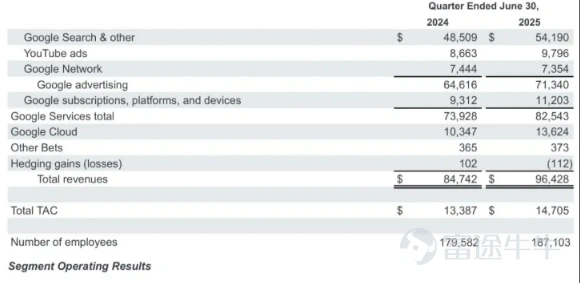

Google parent company Alphabet announces second quarter earnings, revenue and profit forecast to outperform the market. Revenue for the second quarter was $96.43 billion, up 13.8%; EPS was $2.31, up 22% year-on-year. From the point of view of Futubull's performance acceleration function, two people expect the market to be more profitable. THE SHARE PRICE GROWTH AFTER THE OVERNIGHT FALL IS BEGINNING TO CORRECT THE LARGE DECLINE THAT FOLLOWED ON FEBRUARY 5 THIS YEAR, WHICH OCCURRED AFTER THE Q4 RESULTS OF THE 2024 FISCAL YEAR.

$Alphabet-C(GOOG.US)$ The share price has outperformed its share price performance this year, both at the beginning of the year and now or in the second quarter $Nasdaq Composite Index(.IXIC.US)$ (Ending July 23, GOOG YLD up 0.8%, Nasdaq Composite Index YTD up 8.9%, GOOG up 13.7% for Q2, Nasdaq Composite Index up 17.8%). The main reason for this is that Google has a direct input into the development of AI, but the results of this time are conditional and it is beneficial for Google to follow suit over the short line.

First, the main reasons that followed the emergence of Google are two of the technological breakdowns of the AI model (the reason for the replacement of AI's advertising business by AI for years), and the search engine SearchEngine Marketing Business was replaced by AI (May 7, 2017). TODAY'S PERFORMANCE SHOWS THAT THE MARKET IS LOOKING FORWARD TO A REVERSAL ON THESE TWO LEVELS, WHICH WILL BE THE BASIS FOR SUPPORTING THE SHORT-TERM INTRADAY IN THE SHARE PRICE.

Search Business Market Forecast

The Search and Advertising Business continued to grow in the second quarter, with revenue from Search Business at $54.19 billion, up 11.7% year-on-year, well above the $54 billion expected by the market. Total advertising revenue grew to US$71.34 billion, a year-over-year increase of 10.4%, higher than the US$69.7 billion expected by the market. However, the search business is only a small prediction of the market, but the growth rate increases the overall advertising revenue, showing the strength of the search business in relation to AI and has no ambition. The current application and responsiveness of AI is very large, but the complete search business has not become a big trend. For now, LLM AI will not include advertising, short-term internal enterprises are doing digital marketing, Search Engines are trending big, but the main point is flow and performance, for this THERE ARE SIGNIFICANT ADVANTAGES TO YOUTUBE (YT ADVERTISING YOY 13%) AND GOOGLE, WHICH IS A BIG ADVANTAGE FOR WEB BROWSERS.

The Core Business Search Engine is driving SearchEngine's strong performance, which is most likely due to Google's AI Search Product AI Overviews. It now has more than 2 billion monthly active users in more than 200 countries and territories, with an increase of 1.5 billion over the previous year. A large user base leads Search Engines to maintain a strong trend.

Gemini AI in Progress

The news mainly revolves around Google CEO Pichai, during the results conference call, announced several things about the development of AI to highlight:

1. Token Usage Doubles: The May 25 I/O Conference announced that each platform had a monthly token consumption of 480 trillion and processed more than 980 trillion tokens per month in the latest operational data. Doubling in a short period of time indicates an increase in overall demand, which means that more people are using AI models. Reasoning ability will continue to grow as usage continues, benefiting long-term growth.

2. Monthly active users increased: Gemini's monthly active users increased from 0.4 billion to 0.45 billion.

3. Feature Upgrades:Gemini will follow in the footsteps of other AI big models with the introduction of Deep Search, which will increase competitiveness.

AI's products are tough to compete and do nothing to improve Company Valuation.

Capital Expenditure Increase

Finally, we discuss the capital expansion issues of interest to investors in recent years. The company raised its full-year capital base to US$85 billion, up from US$10 billion previously expected. It is important to note that capital support, and not ordinary operational support, is essential support for enterprise expansion business. Only the core business and growth trends are found. An increase in capital support is not necessarily a disaster. Aside from the benefits mentioned above, ROI issues across the AI Industry have eased with heavy use, with news coming that Google Cloud's growth accelerated to 32% this quarter as OpenAI plans to adopt Google Cloud services. AI-Infrastructure Upgrade is a major trend when supported by a large number of requirements. That's why some semiconductors at this point in time, like $NVIDIA(NVDA.US)$ 、 $Broadcom(AVGO.US)$ 、 $Advanced Micro Devices(AMD.US)$ Examples of shares related to Industry Chains, such as $Vertiv Holdings(VRT.US)$ $Oklo Inc(OKLO.US)$ $GE Vernova(GEV.US)$ Another reason for the strength.

Is Yanaga's Target Price Lower?

AT PRESENT, THE GOOGLE SHARE PRICE IS IN THE POST-TRACKING PHASE, AND THE SHARE PRICE IS BEGINNING TO CORRECT THE BEARINGS THAT FOLLOWED ON FEBRUARY 5, FROM A TECHNOLOGICALLY ADVANCED ANGLE, THIS TREND WILL BENEFIT FROM THE SHARE PRICE CHALLENGE TO ITS HISTORICAL HIGHS. Out there, 50 and 200 antennas are correctly prepared to produce a Gold Cross Fork signal on the moving averages, which will benefit the mid-term post-market price performance. Currently, the main resistance position will be at the top of the bearish zone at $203.78, while the key resistance position is at the historical high of $208.21. On the support side, the July 21 Sun trading floor at $187 serves as a reference, only the company remains stable in this regard, and the trend after the share price tracking is maintained.

(Source: Futu Beef Futubull)

In terms of valuation, see on Futubull's Company Valuation function (Shares-> Company-> Company Valuation), with a market price of $191.51 per day, the market rate TTM was last updated to 20.42, below the past five-year average of 26.43, relative to the Reasonable Range (+-1 standard difference))The bottom of the. IT IS EASY TO REFLECT GOOGLE'S CURRENT VALUATION LEVEL, AND THE VALUATION SHOULD BE CONDITIONALLY CORRECTED IF THE CORE UNDERLYING CHANGES FOLLOWING THE SHARE PRICE DEPRECIATION HAVE OCCURRED. However, when corrected to the five-year average of 26.4 per cent, the upside is 29%, and the valuation model calculation above gives the stock a fair valuation of $247. HOWEVER, THIS VALUATION CORRECTION PROCESS IS UNLIKELY TO LAST FOR A YEAR, BUT GOOGLE MAY BE REVISITED AS A MAJOR INVESTMENT TOPIC IN AI'S DEVELOPMENT PATH OR MARKETS AS A MAJOR INVESTMENT TOPIC.

Chief Analyst of Futu Securities Liang

(The author is a licensee of the Securities and Exchange Commission and its affiliates do not have any financial interest in the proposed issuer of shares)