2026 Latest Investment Lazy Bundle

【2025 INVESTMENT DIRECTION】WITH STOCK MARKET REVIEW FOR 2024

2024 is coming to an end. In the last article of the year, the author first reviewed the stock market in 2024 with a graphic and then talked about the direction of investment in 2025.

2025 Investment Direction and Investment Strategy

While U.S. stocks and Hong Kong stocks performed well in 2024, decisions to invest and trade are not easy, and things are subject to slight changes. In conclusion, the author believes that it is most important to understand and judge that your investment trading behavior is logical. For example, assuming a “value investment”, where value investing is concentrated in a few stocks with cheaper valuation potential, this investment concept may be more suitable on the Hong Kong stock market (but this is very difficult due to the complex economic environment. ).

).

As for U.S. stocks, they tend to go “on a rolling basis,” such as investing in the hottest AI topics on the market, or discovering opportunities on the top tech tracks. As long as the physical economy continues to perform strongly, there will always be opportunities for investment or speculation throughout the bull run with technical analysis.

There is really no formula for investing as a whole. Diversified investments are the most effective for individuals who are inexperienced. Chinese assets and US stocks are also worth keeping an eye out for, and do not focus all risks on the same type of investment theme, which is the wind of balancing and lowering The most effective method of insurance.

Stock Market Review for 2024

From the perspective of Futubull's comparison function, the past year has seen the performance of both US and Hong Kong stocks last year.

As of December 20, 2024, the three major U.S. stock indexes have risen over the past year, $Nasdaq Composite Index(.IXIC.US)$ up 32%, $S&P 500 Index(.SPX.US)$ up 25.7%, $Dow Jones Industrial Average(.DJI.US)$ It rose 14.8%. Looking at the performance of the three major indexes, while U.S. stocks performed well in 2024, overall, U.S. stocks in 2024 are unquestionably driven mainly by the technology sector. The topic of AI is the focus of the market, and US stocks are in a bullish mood, and investors are confident that there will be no disputes.

For Hong Kong stocks, the year ended December 20, 2024, for the previous year, $Hang Seng Index(800000.HK)$ It also increased by 17.4%. $Hang Seng TECH Index(800700.HK)$ IT ROSE 18.1%, WHILE TECH STOCKS GAINED MORE, BUT THE MOMENTUM WAS NOT EVIDENT THROUGHOUT 2024. In addition to the good performance of technology stocks throughout 2024, a number of high-dividend stocks were also sought after by funds. However, it is believed that as of today, there is still a lot of controversy in the market over whether Hong Kong shares are in the bull market. The authors can also understand that while Hong Kong stocks rose, the gains throughout the year were mainly concentrated in late January, late April and late September, and the rise was driven by policy.

With this in mind, we first look at the differences between US and Hong Kong stocks to determine our investment strategy for 2025.

US STOCKS CRAZY BULL MARKET SENTIMENT

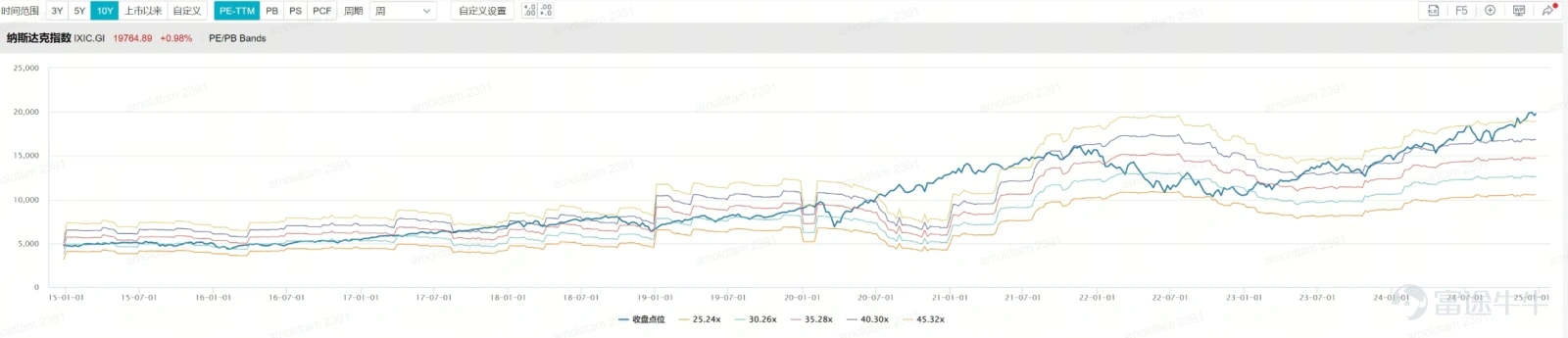

U.S. STOCKS CONTINUED TO PERFORM STRONGLY IN 2024, BUT VALUATIONS ALSO ROSE AND ROSE FURTHER TO HIGHER LEVELS. Continuously high corporate earnings growth is the core logic driving US equities up, but it should also be noted that the rate of increase in valuation levels is also far higher than the rate of corporate EPS, reflecting the valuation of US stocks at expensive levels. AS SEEN IN THE TWO CHARTS BELOW, THE S&P 500 INDEX HAS MOVED CLOSER TO TWO BENCHMARKS THIS YEAR FROM 1.3 OF THE 10-YEAR HISTORICAL AVERAGE OF EARNINGS, AND FROM ABOVE 1 STANDARD SPREAD TO TWO BENCHMARKS ABOVE.

As valuations began to be expensive, there were a lot of market voices suggesting that there was a risk of a bubble in US equities. What made the market deeper was the big drop on Black Monday, August 5. However, with the prospect of a rate cut, US stocks eventually hit the top again. However, there has also been a slight change in the hype of the technology industry, the authors write in” Duma Report Changes Semiconductor Wind Direction, BoE Rebound Should Pick Up” and”US stocks hit back, will the wind change again?” It is also suggested that while the ROI issue of AI is of interest, it is not analogous to the 2000 science web explosion.

After the ROI issue of AI, the market also began to shift towards AI investment, driven by AI 1.0 semiconductors (e.g. $NVIDIA(NVDA.US)$ und $Taiwan Semiconductor(TSM.US)$ ) Hype for changing AI 2.0 power and equipment (e.g. $Vistra Energy(VST.US)$ und $Vertiv Holdings(VRT.US)$ ) After hype, in the fourth quarter it shifted more towards AI 3.0 software categories (e.g. $Palantir(PLTR.US)$ und $Applovin(APP.US)$ ) The hype. This is the main reason why the valuation of US stocks began to move into expensive valuations. Considering the valuation of some software stocks in terms of market capitalization or EV/FTM revenue multiple, this hype tends to push the overall valuation to a very high level, and the profitability patterns of these software companies are always critical to the market expectations.

Finally, with a simple review of the second half of US stocks, there is no major correction in the opinion of US stocks in the second half of 2024.”U.S. stocks continue strong, not to be ignored in the second half” Mentioned in the article $Tesla(TSLA.US)$ 、 $Amazon(AMZN.US)$ und $Coinbase(COIN.US)$ There are also many stories. HOWEVER, THE AI FANFARE AND TRUMP RED SWEEP TRADING IN THE SECOND HALF OF THE YEAR ARE KEEPING AN EYE ON, BUT IT IS INDEED MUCH STRONGER THAN EXPECTED.

Hong Kong stocks are still in anticipation of the worst moment is over

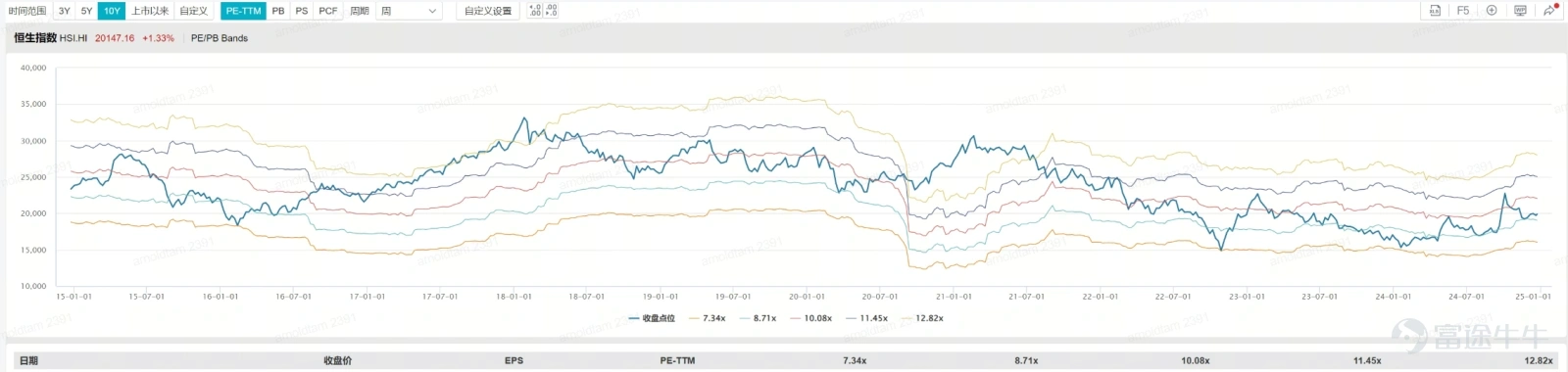

In Hong Kong equities, the Hang Seng index was lower than at the beginning of the year, its valuation rose to one standard difference below the 10-year average. Corporate earnings growth mainly benefited from the “downsizing” of many of the leading companies, which we believe will also be heard frequently in 2024. In fact, many big tech stocks like $TENCENT(00700.HK)$ 、 $MEITUAN-W(03690.HK)$ und $BABA-W(09988.HK)$ It also drove profit growth from gross margins through a series of cost-cutting measures. Even if blue-chip stocks hit all-time highs

$HSBC HOLDINGS(00005.HK)$Breaking historical highs (pre-accounting recovery, net and dividend factors) also drives ROE and stable dividend capacity through corporate restructuring.

However, the practice of “downsizing” is difficult to drive long-term growth in corporate profits, and revenue performance is related to the macroeconomic environment. This is why Hong Kong stocks are still looking forward to a series of fiscal policy initiatives, and the market hopes that the policy will stabilise its economic performance in the coming year. This is the core investment logic for Hong Kong stocks to drive revenue and earnings growth.

If you look at it from the above perspective, it is not difficult to understand the logic of the “bull market” of Hong Kong stocks, which are the characteristics of the “bull market” mentioned by the authors at the beginning of the year.”Is the tech bull market coming to Hong Kong stocks?“。 The authors also mentioned several times in the lecture that “Niuichi” is a typical high-risk and high-return market. For example, the move from 16964 on September 11 to the high of 23241 on October 7, 2024, will have some killing power if the reaction is slow to chase after the highs frequently. “First Half 2024 Review: Is the Hong Kong Stock Bull Market Over? 3 key factors to expect positive results in the second half of the year” This view was not wrong, but the authors were also clouded by the strong bull market atmosphere in early October , resulting in the emergence of both the most successful and the most unsuccessful perspectives of 2024 in this wave

, resulting in the emergence of both the most successful and the most unsuccessful perspectives of 2024 in this wave 。

。

Author Information

Tam Chi Lok

Chief Analyst of Futu Securities

(The author is a licensee of the Securities and Exchange Commission and its affiliates do not have any financial interest in the Proposed Share Issuer)