Futu Research | Does Ailonghead have investment value?

After the close of business on May 22nd, Eastern Time, $NVIDIA(NVDA.US)$FY25Q1 (Natural Season 24Q1) Results Released, Delivered a Surprise Answer to the MarketNVIDIA Stock PriceGained more than 6% above $1,000.

Corporate profits continue to double as a result of the wave of AI change. In the quarter, the company achieved revenue of $26 billion, YoY +262%, diluted EPS of $5.98, YoY +629%, adjusted diluted EPS of $6.12, YoY +461%.

Following the release of the results, the company announced that it will split 1 share into 10 shares, in order to reduce the investment threshold and increase the liquidity of the shares.

Brilliant performance has become historical data and the evolution of stock prices will depend on future growth. Therefore, this article will focus on two core points:

(1) Where is the company's continuous growth momentum and can we continue to support the company's rapid growth?

(2) What is the value of the company's investment?

1. Data center growth is strong, Blackwell chip shipments are expected to drive earnings growth in Q2

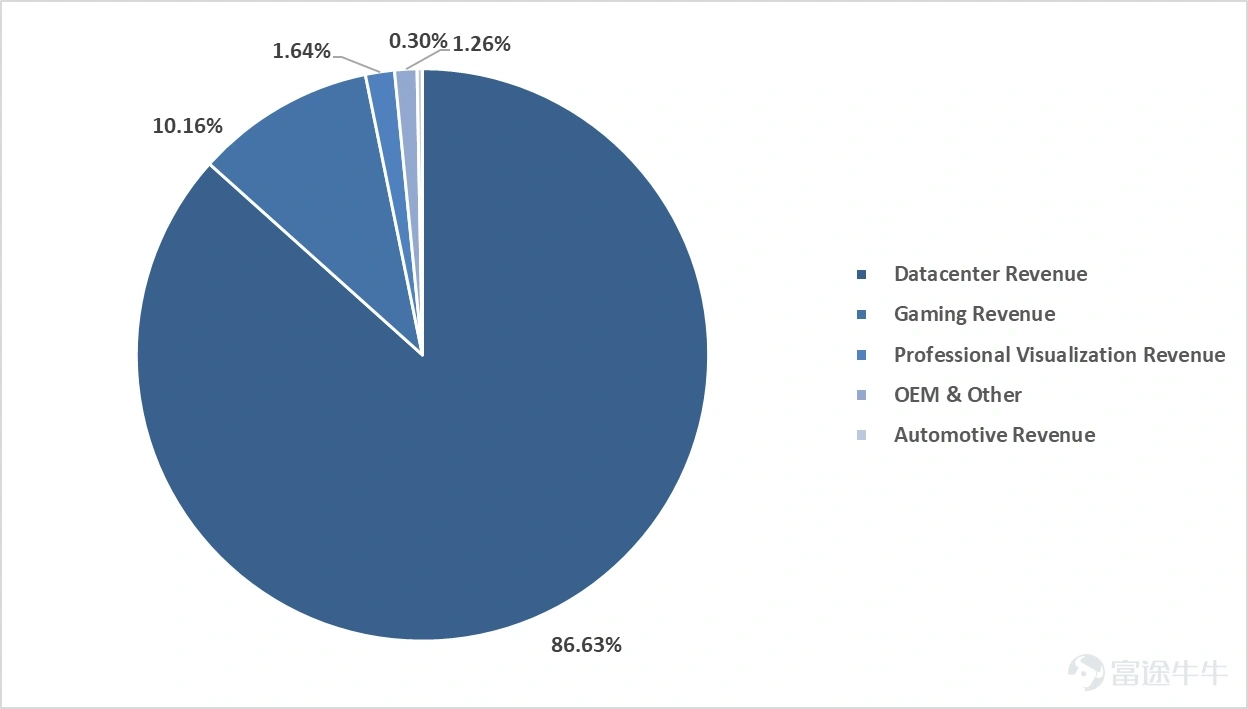

Figure: Revenue composition of Inweida

Source: Bloomberg, Futu Securities Refinancing

Data center business is a major source of revenue and profit at $26 billion in revenue of $26 billion in the quarter, revenue from the data center business accounted for $22.6 billion, YoY +427%, mainly driven by strong and continued growth in the demand for generative AI training and reasoning, especially the overwhelming demand for Hopper chips Shen.

So can the data center business continue to grow at a high rate?

1.AI DEMAND IS STRONG AND CAN BE PRINTED BOTH UPSTREAM AND DOWNSTREAM DATA

(1) From the point of view of downstream customers, Inweida's customers mainly come from cloud services, consumer internet companies, and automotive customers, etc., basically covering global tech giants, including Amazon, Google, Microsoft, Meta, Tesla, etc. And from the quarterly results data, these tech giants have ramped up capital spending to strengthen their AI infrastructure, showing the huge demand for AI chips.

(2) From the point of view of upstream customers, TSMC mentioned after the April sales data release that current AI demand is still very strong. The world's largest chipmaker certifies strong demand for AI, no doubt giving the market a boost.

2. Data center business revenue diversifies, leading AI, network revenue, etc. are expected to become new growth points

(1) The world is upgrading from universal computing to accelerated computing transformation. In addition to Hopper chips, enterprise demand for customized AI services, sovereign country supercomputing platform demand (based on Grace Hopper super chip), NVIDIA AI Enterprise software stack service demand is high, which is expected to contribute to continued revenue for data center business.

(2) At the same time, the first separately announced network revenue of $3.2 billion for the quarter, YoY +242%, thanks to strong growth in InfiniBand end-to-end solutions, is expected to be one of the new growth points for data center business revenue. Spectrum-X Ethernet networking solutions are in mass production with multiple customers and are expected to jump to a multi-billion dollar product line within a year, according to company management disclosures.

In the future, revenue from software services will become a source of income for a longer life cycle of the company.

3. The company has a strong soft and hard competitive barrier, the new Blackwell chips will ship in Q2

(1) The iterative ability of the company's hardware technology is staggering, and the continuous introduction of stronger AI chips leaves competitors far behind. The company announced that Blackwell chips will ship in Q2, increasing production in three quarters and can be deployed in customer data centers in four quarters, which is expected to bring the company a lot of revenue. At the same time, Blackwell chips can be downwardly compatible with existing Hopper architectures, without worrying that the launch of Blackwell chips will cause customers to abandon the purchase of Hopper chips. In addition, the company's management revealed that it will accelerate the update speed of the chipset from a two-year update to a one-year update. Such efficient technology product iterations and updates enable NVIDIA to remain at the forefront of AI chips.

(2) In addition to hardware products, software ecosystems such as CUDA Programming Environment, TensorRT Reasoning Optimization Library, RAPIDS Data Analysis Library are an important part of building NVIDIA's competitive advantage, enabling it to meet enterprises of different industries and sizes for fast response and customized services to complex computing needs, and Improved customer stickiness and increased the cost of customer replacement chip replacement systems.

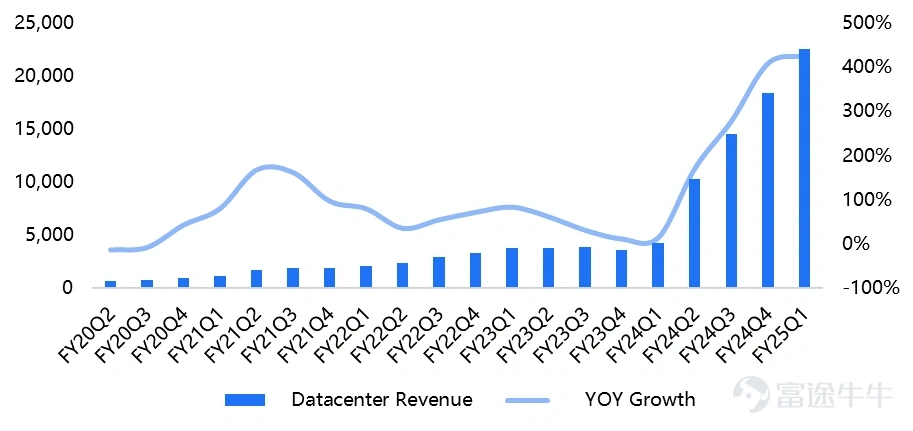

Figure: Data Center Business Revenue (USD Million)

Source: Bloomberg, Futu Securities Refinancing

Second, the game business is anchored by AI PC, professional visualization and stable growth of automotive business

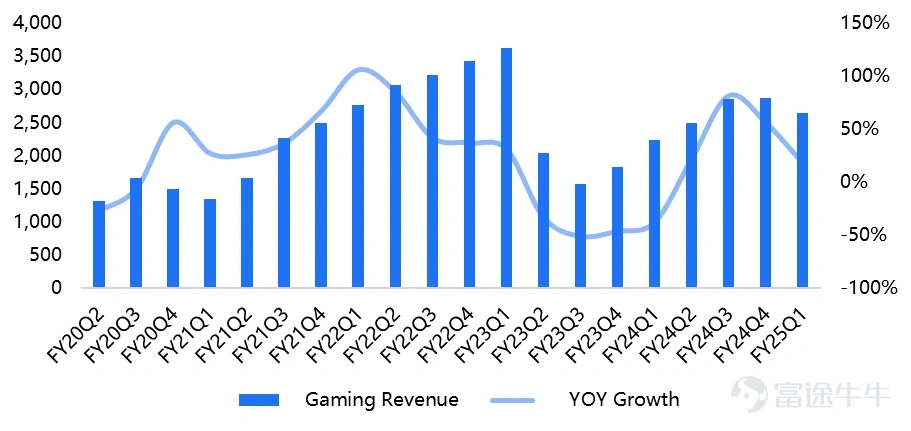

The company's gaming revenue for the quarter was $2.65 billion, up 18% year-over-year and down 8% year-over-year, mainly due to a decline in seasonal sales. GeForce RTX Supers GPU market acceptance is high, and terminal demand and channel inventory across the product line remain healthy.

The future growth point of the gaming business lies in AI PCs. The company has already equipped CUDA Tensor Core in GeForce RTX GPUs in advance, laying the foundation for subsequent AI PCs. Currently, GeForce RTX GPUs have installed more than 0.1 billion, demonstrating NVIDIA's broad user base and strong market penetration in gaming and AI. NVIDIA has a full stack of technologies to deploy and run fast and efficient generative AI reasoning on GeForce RTX PCs. The other day, NVIDIA and Microsoft announced AI performance optimizations for Windows to help increase LLM runtime on NVIDIA GeForce RTX AI PCs by 3x. The growth of the gaming business in the future will be focused on the development of AI PCs.

Figure: Gaming Business Revenue (USD Million)

Source: Bloomberg, Futu Securities Refinancing

Professional visualization and automotive business growth was solid, but the smaller volume had no impact on overall results.

(1) Professional Visualization business revenues of $0.427 billion, up 45% year-on-year, and expected that generative AI and global industrial digitalization will drive the next wave of professional visualization growth.

(2) Automotive revenue was $0.329 billion, up 11% year-on-year, driven mainly by autonomous driving growth, such as Xiaomi's first electric car SU7 powered by the NVIDIA DRIVE Orin autonomous driving platform. The new generation of autonomous driving platform NVIDIA DRIVE Thor will adopt the new NVIDIA Blackwell architecture and is expected to begin mass production next year.

Third, there is still room for improvement in gross profit, and shareholder returns

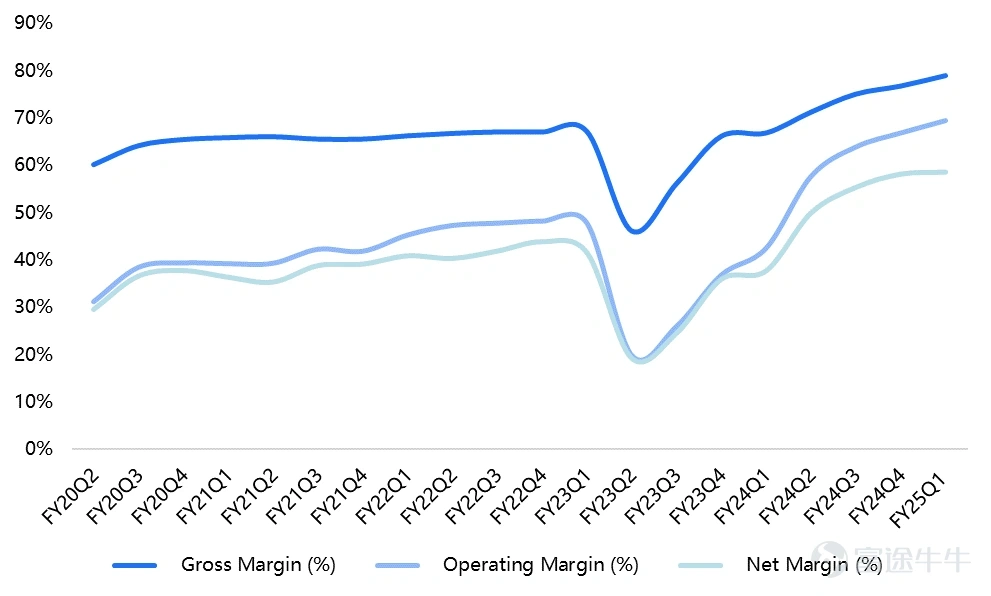

Gross profit hit a new all-time high, and EPS has doubled in consecutive years. The Company's GAAP gross margin for the quarter continued to increase to 78.4% and non-GAAP gross margin to 78.9%, a marked increase mainly due to high gross margin Hopper GPU chips, lower inventory costs and lower upstream component product costs. EPS doubled, diluted EPS of $5.98, YoY +629%, adjusted diluted EPS of $6.12, YoY +461%.

Figure: Profitability

Source: Bloomberg, Futu Securities Refinancing

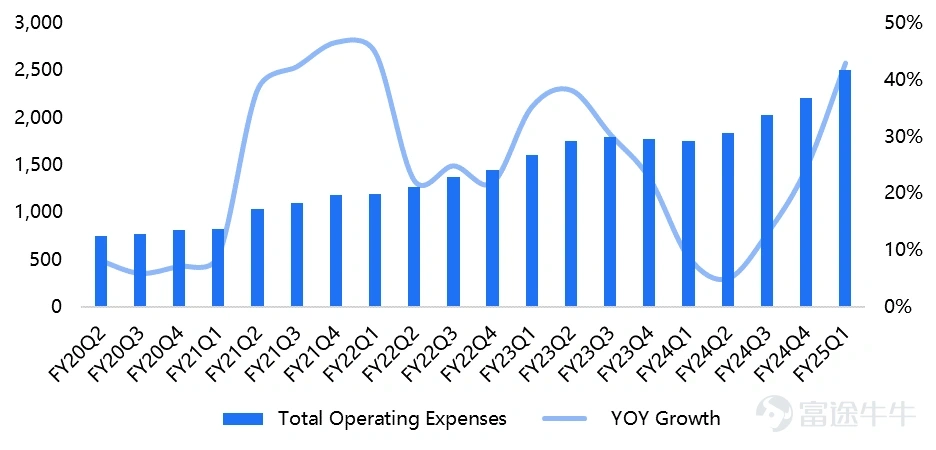

The operating expense rate is low, and the cost control is excellent. Operating expenses for the quarter increased 39% year-over-year and adjusted operating expenses increased 43% year-over-year, driven primarily by pay and benefits, reflecting growth in employees and remuneration. However, the overall operating expense ratio fell to 13.4%, reflecting the company's excellent cost control capabilities and further dilution of costs as a result of scale.

Figure: Total Operating Expenses (US$ Million)

Source: Bloomberg, Futu Securities Refinancing

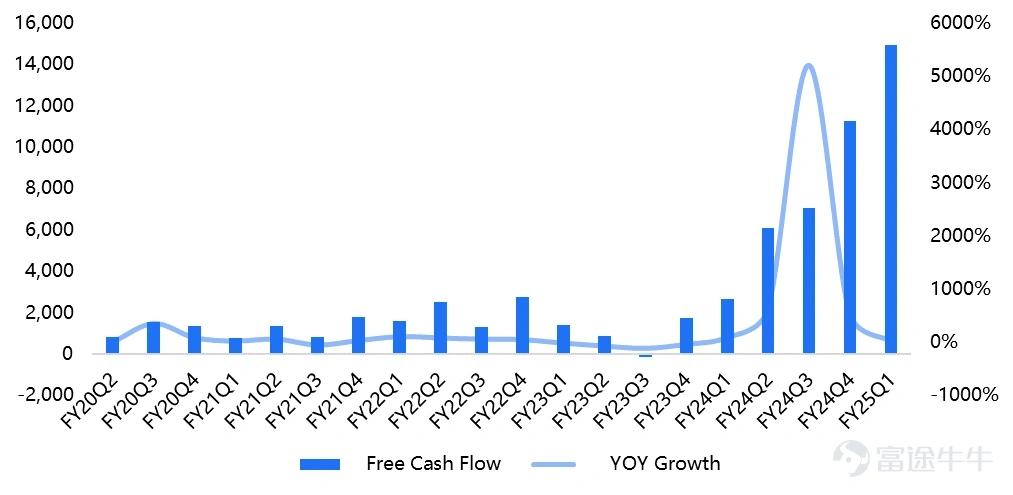

Free cash flow is growing strongly and free cash flow is expected to exceed $60 billion for the year. With the rapid growth of the company's net profit, the company's free cash flow for the quarter was $14.936 billion, YoY +461%, and is expected to have more than $60 billion in free cash flow in FY25. As of FY 2024, the company's cash and cash equivalents stood at $31.4 billion, up from $15.3 billion in the same period last year and $26 billion in the previous quarter.

Figure: Free Cash Flow (USD Million)

Source: Bloomberg, Futu Securities Refinancing

There is still room for improvement in shareholder returns. Returned $7.8 billion to shareholders in the quarter, including $7.7 billion in stock repurchases and $98 million in dividends. The company currently has a residual repurchase size of $14.8 billion, while the company announced a 150% increase in the quarterly cash dividend from $0.04 per share to $0.10 per share. The expected return to shareholders for FY25 is at a relatively low level of 1%. With free cash flow expected to exceed $60 billion in FY25, there is still room for improvement in shareholder returns.

4. What is the investment value of Inweida?

Overall, Inweida continues to benefit from growing AI demand, with record growth in its business size and profitability. With its hardware technology advantages and CUDA ecological advantages, NVIDIA expects to maintain its absolute market position in the fierce competition.

1.EPS

The company's results are expected to continue to grow at a high rate, driven primarily by revenue growth in the data center business. The reasons include several critical factors mentioned above:

(1) AI demand remains strong through upstream and downstream data printing.

(2) Data center business revenues are becoming more diversified. In addition to hardware chip sales revenue, Sovereign AI, Enterprise AI Services, AI Enterprise Software Stack Services, Network Solutions Revenue, etc. are expected to be new growth points. Future software service revenue is expected to be a source of revenue for the long life cycle of the company.

(3) The company has a strong barrier of soft and hard competition. Hardware technology and product acceleration iterate, the update speed of chipsets accelerates from a two-year update to a year-on-year update, and the new Blackwell chips will ship in Q2, keeping the lead in the AI chip space. AT THE SAME TIME, SOFTWARE ECOSYSTEMS SUCH AS CUDA HAVE IMPROVED PRODUCT ADAPTABILITY AND IMPROVED CUSTOMER STICKINESS, INCREASING THE COST OF CUSTOMER SWITCHING CHIPSET SYSTEMS, BECOMING THE COMPANY'S MAIN COMPETITIVE ADVANTAGE.

Based on the company's performance guidance, FY25Q2 median revenue is forecast to be $28 billion, above market expectations. GAAP and non-GAAP gross margins are 74.8% and 75.5%, respectively, with full-year gross margins expected to be around 70%. In addition, operating expenses are expected to grow by around 40% throughout the year.

Considering the start of Q2, the company's EPS growth began to double, and EPS growth is expected to slow gradually after the second quarter of FY25. Overall, with strong AI demand and excellent cost control, EPS growth is expected to grow at around 100% for FY25.

2. Return to Shareholders

The expected return to shareholders for FY25 is at a relatively low level of 1%. With free cash flow expected to exceed $60 billion in FY25, there is still room for improvement in shareholder returns. Assuming full cash flow is excluded, the FY25 shareholder return is expected to reach 2.56%, which is still not high.

Therefore, the momentum of the increase in the share price of the shares depends mainly on the rapid growth of the results, and whether the growth rate can be sustained will significantly affect the share price of Indira. A negative impact on valuations will have a negative impact on the valuation once it slows down. We expect FY25 EPS to grow twice as measured by a share price above $1000 after the results, with the current PE valuation at around 35-40x, which is relatively reasonable and still able to support the current share price.

AI is a long-term trend, and the value of long-term investment is beyond doubt as the “shovel seller” in the AI industry. Today's investors need to pay more attention to whether more cutting-edge technologies and broader needs emerge in the AI sector that can drive the growth of the AI industry, thereby enabling the continued benefits of NVIDIA. Be alert to the risk of slowing demand, increased competition, and technological alternatives.